Health Spending Accounts For Canadians Explained

A Health Spending Account (HSA), also known as a Health Care Spending Account (HCSA) or Health...

By

October 19, 2021

By

October 19, 2021

A Health Spending Account (HSA), also known as a Health Care Spending Account (HCSA) or Health Reimbursement Account, is an individual account with a fixed dollar amount used by employees and/or their eligible dependents for reimbursement of health and dental-related expenses not covered under provincial health insurance or other group benefit plans sponsored by the employer.

In Canada, HSAs are tax-free in most cases (with the exception of Quebec), meaning employees and covered dependents use pre-tax corporate dollars, from an HSA 'bank', to pay for medical bills that would normally be an out-of-pocket expense.

HSAs are an effective way to give employees more flexibility in how they use their benefits as the scope of what can be reimbursed is much broader than what is typically covered under a traditional plan.

Expenses that can be claimed through an HSA are dictated by the Canada Revenue Agency (CRA) and are the same as the medical expenses that could otherwise be claimed on an individual's tax return.

Here are examples of expenses that can be claimed through an HSA:

It's important to know there is no insurance protection for catastrophic expenses or out-of-country coverage with an HSA. Once you've hit your allocated HSA limit, you're done. A traditional group benefits plan can provide this.

An HSA can be offered by the employer in two ways: on a stand-alone basis, or as part of a group benefits plan. The financial responsibility of the employer and employee varies depending on the implementation of the HSA.

1. Stand-alone HSA (aka Private Health Services Plan/PHSP):

2. HSA as part of a group benefits plan:

In both cases, the HSA 'bank' balance decreases as claims are reimbursed until the balance reaches zero.

The employer has these options for handling unused funds and/or expenses at the end of the year:

In the Simply Benefits platform, we make it easy for members to submit claims through their HSA. See how:

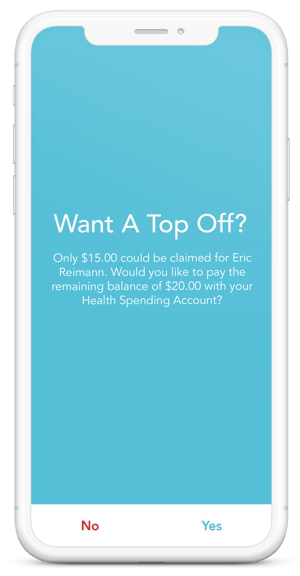

Quick Tip: In the Simply portal, for members that submit a claim through their traditional plan first, they can submit any unpaid amount automatically (in one claim) through their HSA by choosing the Top Off option(see screenshot below). Members are typically are reimbursed within 48 hours.

Though they may sound similar, a Health Care Spending Account and a Lifestyle Spending Account (LSA) operate differently. Unlike an HSA, an LSA is considered a taxable benefit. The employer decides what lifestyle expenses will be reimbursed, and after-tax dollars are used to cover the products and services. Commonly reimbursed expenses are non-medically required products and services that fall under categories such as:

Given the tax-free benefits, Health Spending Accounts are a great option for any business looking to provide their employees with health and dental benefits. Further, as new generations continue to enter the workplace, spending accounts are becoming increasingly popular. Stay on top of the trends with more information on the type of benefits that millennials want.

If you don't offer a Spending Account already but would like to, it's easy to add! Just speak with your benefits advisor to set one up. If you need an Advisor, contact us and we'll introduce you to one of our partners.

Contact the Simply Benefits Support Team.

Simply Benefits providers both Health Spending Accounts and Lifestyle Spending accounts. Speak with our sales team to learn more.

If you're an employee looking for help to better understand your group benefits plan, check out these resources:

Simply Benefits is Canada's newest Third Party Payor (TPP) that provides Employee Health Benefits 100% digitally through our Canadian Advisor partners. Our all-in-one digital solution provides three portals that enable Benefits Advisors to digitally manage all client plans online, Employers to efficiently administer employee coverage, and Employees to view, update and use their benefits 24/7 via desktop or smartphone app.

We help ENGAGE Employees Anytime, Anywhere, SIMPLIFY the Benefits Experience, and EVOLVE an Advisors’ Benefits Business.

Connect with us at simplybenefits.ca or on LinkedIn, Twitter, Facebook, Instagram, and YouTube.

Employee Benefits Made Simple.

Terms + Conditions

Simply Benefits Inc. (“us”, “we”, or “Simply Benefits”) is committed to privacy and the protection of your information. By using Simply Benefits’s website, mobile and other applications, and related Services made available through the Apple App Store, the Google PLAY Store, or otherwise on the Internet (together, the “Simply Benefits Applications” or “Applications”), you acknowledge that you accept the practices and policies outlined in this Privacy Policy (“Privacy Policy“). Unless otherwise defined herein, capitalized terms shall have the meanings assigned to such terms set forth in the Terms of Service and which incorporate this Privacy Policy by reference.